Four out of five people agree there’s a housing crisis.

Crisis means different things to different people, but a recent survey revealed the root is the same: decent, affordable homes are becoming harder and harder to find.

What is more surprising perhaps is that four out of five people would also accept more development where they live, so maybe we’re not a nation of ‘not in my back yard’ after all. We’ll need that local support for housebuilding given we need around 300,000 new homes each year, double the levels we’re building right now.

I feel like I’m never going to be able to buy a house and that scares me. What happens when I retire?

Female, 25-34, south east, private rent

And the survey says…

And the survey says…

I’ve worked in housing for many years now, and I’ve seen how something as simple as a house is intrinsically bundled up with people’s emotions, their aspirations and their financial security.

It’s not just a castle for an Englishman. It’s a bank, a springboard, a safety net, an investment, an inheritance, a pension.

So I decided to carry out a survey. As house prices cannot carry on booming, I particularly wanted to track the trends as the market shifted, but mostly I wanted to hear firsthand what housing meant to people.

I had around 140 responses, mostly through Facebook and Twitter, spread right across England and Wales, from homeowners to renters, from families to singles.

The majority were in the south east and I appreciate it’s a small sample size. But what was most eye opening were the individual stories that people shared. Housing, the place we call home, is so vital to our quality of life.

I was homeless for 3 months last year! The b&bs around our area were bursting at the seems. My housing officer said its the worst they’ve seen since they’ve worked here.

Female, 35-44, Yorkshire and The Humber, private rent

When is a crisis a crisis?

A third (32%) of respondents said they were worried about keeping up with their mortgage or rental payments.

Given record-low interest rates, this was higher than I was expecting. But, on average, houses cost first time buyers 4.5 times average incomes in the south east – up from 2.6 times in 1996.

Where I live, a 3 bedroom home can cost £500,000.

Getting on the property ladder to be a first time buyer is near on impossible despite good incomes the deposits are astronomical.

Female, 25-34, south east, social/affordable rent

And low rates often benefits those with a home, bought a lower price and with some equity. Those buying at a peak of house prices will take on a larger debt, albeit at low rates. Should rates rise payments will quickly become more difficult to meet.

(Note: the survey was before the EU referendum, so people may feel more secure if rates stay low or fall as they’re expected to in the short term.)

As well as house prices, rents have been on the up over the last few years (as the graph shows below), while wages haven’t kept up.

What should government do?

Government has always been interested in the housing market. It impacts on jobs and economic growth, consumer confidence and spending, social mobility, health and education – it affects the income government can receive from taxes and it simply makes people feel wealthy. It’s importance is not in question, but where government gets involved – or leaves to the market – varies greatly.

The survey question assumed that government would invest in housing, and respondents were split fairly evenly on where they thought they should put the money.

Not surprisingly affordable homes to buy topped the shopping list, but affordable homes to rent was seen as a slightly greater priority than helping first time buyers.

Perhaps, the solution is about combining cheap, long-term finance options for those starting out with building more homes that everyone can afford, from first-time buyers to those looking for the home for life.

It was reassuring to see tackling homeless was a priority given the survey was an exclusively housed group of people. But interestingly private rent was low down the list, as was older person’s accommodation.

Perhaps the reason for the latter was because most respondents fell in the 24-45 range, but the issue of decent, affordable housing – with the right level of care and support – will only get more important as our population ages.

What are housing associations for?

I work for a housing association, and have been in this sector for about seven years now.

Since I’ve been here there’s been a concern that the sector doesn’t have a unified voice, a single elevator pitch for what it’s for.

This is reflected in the words people used to describe housing associations (left). People know we provide affordable homes, they know we’re ‘social’ or charitable and many are positive about the difference they make.

This is reflected in the words people used to describe housing associations (left). People know we provide affordable homes, they know we’re ‘social’ or charitable and many are positive about the difference they make.

When asked about where their priorities should lie, while being a good landlord was the main focus, they recognised housing associations role in building new homes too.

Interestingly, and probably not surprisingly however, people didn’t see helping those on middle-incomes as such a high priority. These housing options, such as shared ownership and private rent, do meet a need (people on middle incomes can also struggle to buy a home while some want the flexibility that comes with renting).

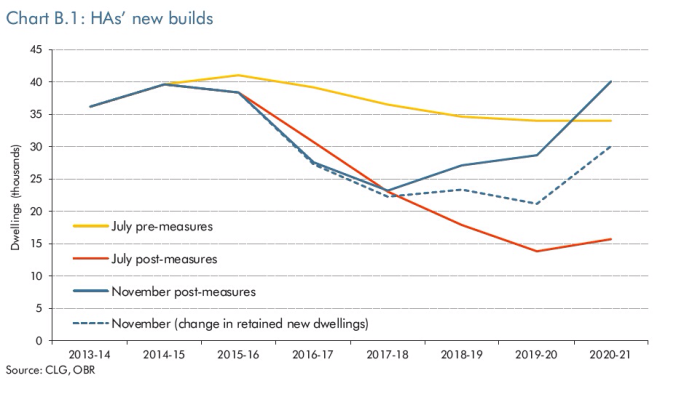

While you can argue whether it is for housing associations to meet these needs, the truth is that to build more affordable housing, housing associations have had to change how they operate. In the past, housing associations would have received government grant to subsidise the construction of a home so it can be rented at sub-market rents. This grant has all but dried up, so housing associations have been adapting, seeking other sources of finance to keep the building going.

While you can argue whether it is for housing associations to meet these needs, the truth is that to build more affordable housing, housing associations have had to change how they operate. In the past, housing associations would have received government grant to subsidise the construction of a home so it can be rented at sub-market rents. This grant has all but dried up, so housing associations have been adapting, seeking other sources of finance to keep the building going.

Selling properties and providing more homes for private rent is one way to bring in more money to replace the grant. This income then makes it possible for housing associations to build more affordable homes and provide services for those that need them.

Housing associations provide a vital safety net for vulnerable people.

Female, 35-44, London, own – mortgage

Housing associations may not always get it right but they are doing their best and have a hugely important role in helping people who are usually doing their best to get on in difficult circumstances.

Female, 45-54, south east, own – mortgage

How to solve the housing crisis

We’re not building enough homes, many are not available at a price – to rent or buy – that people can afford and that meet the needs of our changing and ageing communities.

There is no way the housing crisis will be solved, as no-one is doing enough about it – government, housing associations or councils.

Male, 25-34, South East, private rent

The main levers government has to affect housebuilding are planning, investment and regulation.

But getting the balance right, given financial and political constraints, is the challenge. If you bring one down, you need to dial others up. For example, if you reduce investment you could mitigate the impact by removing planning restrictions and red-tape. But you don’t want to reduce it too far or you could impact the quality of the homes or not build the types of homes that meet the broad range of needs in an area.

Government can try to force those who can build but don’t (or are not building the type of housing needed, or not quickly enough) while incentivising those that want to build, but can’t.

I believe that housing associations have a big role to play. Last year the top 50 housing associations built 40,000 homes (Subscription required). This is a decent effort, but we need to go much further.

I disagree with the respondent that said government, housing associations and councils don’t want to solve the housing crisis. They all do, and, in difficult and uncertain circumstances are doing what they can to build more homes.

But what struck me most from this survey, which came through strongly in the individual stories, is how many different types of crisis’ there are. Every person, couple and family, at each stage of life need a safe and secure home.

The challenge is knowing which crisis to solve first.

An article in the Guardian this morning, written by a council housing employee, talks about the importance of frontline social housing employees in building a better housing future – I couldn’t agree more.

An article in the Guardian this morning, written by a council housing employee, talks about the importance of frontline social housing employees in building a better housing future – I couldn’t agree more.

Housing probably seems pretty dull right? But we all want a safe and secure place to call home don’t we? Without it, everything else just doesn’t work.

Housing probably seems pretty dull right? But we all want a safe and secure place to call home don’t we? Without it, everything else just doesn’t work. We’re very lucky to have a democratic political system, where we all get a say in who represents us in Parliament.

We’re very lucky to have a democratic political system, where we all get a say in who represents us in Parliament.

2015 was an unpredictable year.

2015 was an unpredictable year.